Property Taxes in Turkiye

Tax Laws and Regulations have changed again in Turkiye for 2026 and will continue to do so... For that reason please seek advice directly from a specialist... for insights on how to do this simply and cost effectively, MyTapu Associates provides general guidance ....General Tax information is below...and most likely now out of date... Do not rely on internet sources. Seek qualified professional advice. Specialist Tax Accountants, not lawyers, provide these services in Turkiye, but lawyers also provide specialist service and representation... How to choose ? Email us today at info@MyTapu,com. .

Tax Free for Twenty Years ?

There is much discussion about new proposals for enticing foreign investors by offering twenty years of zero tax rate on foreign sourced income. This proposal is not receiving detailed commentary just yet on these web pages because:

There is much more talking between politicians needed before anything happens;

- Turks that do not reside in Turkiye more than 90 days consecutively in a 180 day period do not pay tax on foreign sourced income anyway, so any foreigner doing the same, will not either, and if the foreigner obtains a Turkish residency permit or passport, the same applies.

- With proper advance planning a foreign person acquiring Turkish residency and /or passport can arrange their lifestyle for better advantage and lower taxes anyway. For example, spending time two hours drive from Istanbul in Turkish speaking Southern Bulgaria, the tax rate is only 10%, but if the person is of a pensionable age (there is great flexibility) there are techniques for reducing the income tax rate to zero; in Greece, also two hours drive from Istanbul, or a 40m ferry boat ride to multiple island choices, it is possible for foreign residents to reduce their tax rate to 6% under various schemes; in Turkish Republic of Northern Cyprus, a ferry boat trip or quick flight hop from Turkiye, there is also an advantaged tax regime for Turkish residents and passport holders.

Property Title Transfer Tax...

Turkey's Revenue Administration is now issuing penalties and interest on under-paid Tapu Harcı- the 4% transfer tax on title deeds that is paid at land registries based on the declared sale/purchase price of a property. Avoid penalties, interest and a Tax Investigation arising from past underreporting of transaction prices, with a legal process within article 371 of the the Tax Procedure Law, known as voluntary disclosure.

Property Owners' Tax Alert....

This tax is mentioned here, at the top of this page because...

- This tax is accruing an interest penalty at 4.5% monthly (54%+ yearly)...

- ... and no one is talking about it so non-Turkish property owners are generally unaware of it... !

- The solution does not require a registered tax accountant to remedy....

For Buyers

Transaction Tax of 4% is a Liability Shared Equally by Buyer and Seller at 2% each

How does understating the price declared at the land registry for less than the real property purchase price result in higher transaction taxes payable ? The Tax Man assesses the amount of transaction tax under-paid, and charges 4.5% monthly (54% + yearly) annual interest penalty – so the amount of underpaid transaction tax liability more than doubles every two years, PLUS an additional penalty charge. So the buyer ends up paying the transaction tax anyway, plus the interest, plus the penalty.

Even if the buyer has paid the seller's 2% transaction tax, the 2% liability on the understated purchase remains.

For Sellers

Transaction Tax: Before selling the property, all taxes must be paid – and that includes the transaction taxes payable arising from understating the declared value on the Tapu at the land registry below the real purchase price, at the time of purchase. Not only is a penalty payable, but also, that tax liability is increasing at 4.5% monthly (54% + yearly)….

Capital Gains Tax: How to reduce your capital gains tax liability when selling a property before the five year exemption period ? if you understated the declared value to be less than the real price at the time of purchase, follow the solution below in the Guide....…

Your First Potential Buyer - A Private Conversation... The advice under this heading on the page here and on the following link is so important it may be considered essential... read it here...

'Why do I have to pay Property Tax Penalties on my Tapu in Turkey...? '

Most property owners in Turkiye will usually remember paying a much higher price for their property purchase than the value declared at the Land Registry and showing on their Tapu....

Owners may be surprised to learn that the Turkish tax man is levying :

1) a penalty, and

2) claiming the underpaid tax, and

3) charging interest on the amount of property transfer tax unpaid (on the difference between the real transaction value purchase price, and the under-declared value).

The amount of interest charged is 4.5% monthly, which is more than 54% yearly with compounding.

A better explanation is in the video above.....

- For the solution with detailed step-by-step Do-it-Yourself advice and guidance, please see below and request the Guide... 'Avoid the Penalty'... email info@mytapu.com. with the subject... "Avoid the Penalty' to request the Guide

'Hiding & Hoping' the tax man won’t find out, isn't a solution.

So your agent says the taxman has no way of knowing how much the real price you paid was ? That answer is just another misleading diversion…

Yes, the taxman will get his money, and has means of 'guess-timating' the true transaction price- this price will be his ‘assessment' - arguing is futile.

How will the taxman know the true price paid?

- He doesn't have to know- instead calculating an assessment....

- His assessment decision is final.

- There is no legal scope for recourse through the courts to challenge the taxman's decision- tax court recourse is purely 'notional'.

Historical Price Data: The taxman may base his assessed value on several sources of existing digital data base information:

a) Since 2003 from the military permit application;

b) From 2007 from mortgage applications that include down-payments and final payments, and ekspert appraisal records;

c) Since 2013 from the digital databases of on-line portals.

These data sources have extensive price information for every nook and cranny of the Turkish real estate land scape, and the Tax authorities have combined all into a new cross referencing analytical system called 'MEVA' (Mekansal Veri Analiz Sistemi).. .

With these sources of data the calculations can easily be made to index the depreciation of the Turkish Lira against foreign currencies.

Yes, the information is available from sources other than the land registries....

'Hiding & Hoping' the tax man won’t find out, isn't a solution.

More than 2,500 owners have done the smart thing and paid already, avoided the PENALTY and STOPPED the interest… so should you, too... and NOW... delaying is just costing more in interest…one percent more every week ! That’s EUR 50 a week for a EUR 5000 tax liability amount... every week ! .

Getting caught and fined the penalty = and interest accrued at 54% per year- is inevitable- as the taxman introduces systematic checks to apply the assessment at the time of twice yearly payments for annual property taxes. The exact timing of the systematic checks is likely to vary, for each local area tax office, In the same way that enforcement compliance is now imposed for 'habitation certificates' ( correct term: Building Utilisation License Certificate: Yapi Kullanma Izin Belgesi aka 'Iskan').

Once caught, and fined the penalty, expect an additional interest penalty on the penalty fine ( standard procedure ! ).

Best advice is to begin payment preparations now (local bank credit loan ?- may be a good 'deal' if the interest rate is below 54% !!!) and make the payment now to avoid the penalty and interest – get the ‘Guide' for the Easy ‘Do-it-Yourself’ steps, and save accountant’s fees too...

The Good News is...in the ' Guide, Avoid the Penalty'... get it now !

The good news is... in the 'Guide' ... see below.

- The amounts involved are not huge but also not 'throw-away' money.

- The solution requires a procedure that may be completed in a few days to a few weeks (depending on each case and the TaxMan) that is relatively simple and the 'Guide' can show you how to do it yourself.. and save without paying fees charged by Tax Accountants..

- The simplest and most practical solution is explained in the D.I.Y. do-it-yourself Guide below... 'Avoid the Penalty'.

Begin the process NOW to allow ample time to complete, before next tax investigations at the time semi-annual property payments are due in November…

Get the Guide to Avoid the Penalty and Stop Interest at 54%+

The Guide:

- Simple 'Do-it-Yourself' steps...

- Save on Accountant's Fees...

- Save on the Penalty Amount...

- Save on the Interest Payments...

- Avoid a Tax Investigation by the Inspector

Estate Planning: Essential Best Investment for Estate Planning Purposes

For Estate Planning Purposes, this is the single best use of first available funds, because finding an alternative government guaranteed investment that yields 54%+ per annum is highly improbable.

My Tapu's Property Taxes...

Yes, annual property taxes are increasing due to official increases in appraised values, which have been artificially low for several years, partly because of the annual rate of Turkish Lira currency devaluation, and inflation ....

Get the Guide Today...

email info@mytapu.com with subject 'Avoid the Penalty'...and the 54%+ annual interest...( !!! )

Follow the Key Insights of How to Simply Do-it-Yourself in the Guide...

Tax related to property and real estate in Turkey concerns;

Tax related to property and real estate in Turkey concerns;

a) Tax declarations and documentation are required on the purchase of every real estate transaction in Turkey prior to the transfer of title ownership;

b) Tax declarations and documentation concerning rental income and income tax payable are required upon filing and payment of annual property taxes..

c) Tax payment receipts and documentation, including capital gains tax, and now the transaction tax and penalty and interest fine arising from under-declared original purchase value, are required from the seller for every real estate transaction in Turkey prior to the transfer of title ownership.

The Tax Experts designated at mytapu.com are licensed and certified to represent clients' tax affairs the Ministry of Finance, in Turkey, and are experienced representing foreigners owning property for many years.

Property Related Taxes in Turkey

Taxation of property related matters in Turkiye is a specialist area outside the scope of the Transaction Management advisory services provided by the experts at MyTapu Associates.

MyTapu provides referral services to qualified and licensed tax experts - please email info@mytapu.com for additional information. .

No one should rely on information provided by estate agents, international property or citizenship websites found on the internet, doing so will be very costly in terms of incorrect information, oversimplified, mis-leading etc leading to penalties and unpleasant surprises.

Expert taxation advice is essential because:

1) the tax regulations change continuously

2) each tax payer's specific circumstances are different and generalisations may often be misleading

3) only a licensed expert can be relied upon, and may also provide solutions not otherwise known.

A tax expert licensed to represent a client's tax returns and affairs to the Ministry of Finance is known by the title of a Mali Musavarlik.

The experts MyTapu refers clients to are:

a) licensed and prequalified to ensure compliance with MyTapu's policies of best practice and client care;

b) English speaking and servicing;

c) Fee checked to ensure fees are charged at market prices and not at the over-inflated prices charged to non-Turkish speaking clients.

Taxation in Turkiye may be using similar terms to those in other countries but the manner applied may be different.

New regulations governing short term property rentals as of January 2024 will have specific implications for property owners tax liability. Click here for a brief look at some of these issues related to new short term holiday rentals.

The Key to Successful Investment

Presuming knowledge and experience gained from other countries is applicable in Turkiye - is the single largest cause for investment failure. Differences in law, land registry practices, tax, accounting, banking, cultural and especially local business practices, do impact investment results. The key is to prevent years of troubles, before buying... All successful investors apply a fundamental discipline that is The Key ingredient of success...

What Investors Say About Us

Investment in residential property in Turkey by International Buyers has been permitted beginning in 2007. Since that time My Tapu Associates have served more than three thousand investors with the advice needed to avoid typical dangers and make their investment a success... See what insights Investors share about buying and selling property in Turkiye, and the value of our Independent Professional Advisory Services (not real estate commission services) here.

Privacy Protection

Is Your Right...

Does anyone want to share private questions & answers with ChatGPT ? To train and share with the world...? For private issues, confidentiality matters, and Venice-PRO.AI has the

Effective January 1, 2026 new Land Registry regulations for property purchase and sale transactions...

For Buyers AND Sellers: New Regulatory Requirements:

- ALL payments to be made by bank transfers directly to Land Registries’ on-line banking services

- Checking of transaction price declarations, contract prices, and payment amounts - must all be the same

As an Example of How the Regime and System is applied....

In Turkey, income tax rates are applied progressively by taking into consideration the yearly cumulative income tax base. Income tax is paid at the highest marginal bracket rate. Rental income derived from property located in Turkiye is subject to income tax. Capital gains on property sales realised before the five year holding period are taxed as income. Allowances may be applied. .

All information on taxes shown below is subject to change without notice. Please seek expert advice from a qualified tax advisor.

Non-resident individuals are liable for income tax only on income earned in Turkey.

Foreigners are regarded as resident if they stay in Turkey without interruption for more than six months in a calendar year.

Income tax is charged on a trade or business, employment, professional services, dividends and interest, agriculture and rentals.The residency rules and taxation rules change continuously and so expert advice is essential.

The general rule is that taxpayers must remit the amount of tax due in two equal payments. Taxpayers carrying on business or professional activities must make quarterly income tax payments during the tax year.

Income from the sale of immovable property within 5 years from the date of acquisition will be subject to income tax, which is determined as the capital gain between the purchase price stated on the tapu, and the sales price stated on the tapu. An expert can advise the inflation indexation applicable, if any.

As an example, subject to continuous updates for which expert advice is essential, in determining the taxable capital gain, the acquisition cost is adjusted for inflation by the increase in the producers' wholesale price index between the date of acquisition and the date of sale. This adjustment can be made if the rate of increase in the wholesale price index for the period concerned is 10% or above, but the acquisition cost may not be adjusted for price increases below 10% for the purpose of determination of taxable capital gain. Net taxable capital gain is calculated by deducting the acquisition cost (inflation adjusted) and the expenses incurred/duties paid by the seller to realise the sale transaction.

Tax Deductions and Allowances - Available deductions depend on the type of income. For business income, the same general deductions as apply to corporations are available. If a proeprty owners rental income is to be taxed as business income with applicable allowances, expert advice is essential.

Real Property Tax - Real property tax is levied based on the value of the land or buildings. For residential property these are determined by the local government authority. In practice, these declared valuations are substantially below current market values. Property tax is calculated in respect of each property at the tax value set at the year of acquisition, which is then revalued annually with the half of the revaluation rate announced by the Ministry of Finance. The rate of the tax on the taxable values of buildings is 0.1% if the building is used as residence and 0.2% for other buildings. The rate of tax on the taxable values of property in lands is 0.3%. These rates will be doubled in metropolitan areas.

Real property tax paid by individuals deriving business income is deductible from the income tax base for commercial business activities, provided the property is recorded as a business asset. Individuals that derive rental income from real estate also may deduct the real property tax paid in determining the taxable amount of rental income.

Turkey Tax Year- Turkey tax year is calendar year or fiscal year.

Filing and Payment of Tax - An income tax return must be filed by all individuals that derive business or professional income. For other types of income (e.g. salary, income from securities, income from immovable property, capital gains, etc.), the obligation to file an annual return depends on the type of income, the amount, and the exemption limits applicable. Individuals who are required to file an annual income tax return must submit the return between the first and 25th day of March of the following calendar year. Income tax accrued must be paid in 2 equal installments in March and July.

The standard rate of VAT (Katma Deger Vergisi - KDV) in Turkey is 18%, with reduced rates of 8% applicable to basic foodstuffs, tourism services; pharmaceutical products and other items, and 1% for journals, newspapers and certain farm products. Certain supplies are exempt.

Filing and payment of tax VAT payments are due monthly. VAT returns must be filed with the local tax office by the 24th day of the following month and VAT is payable by the 26th day of the month in which the return is submitted.

Registration- There is no turnover threshold for VAT registration in Turkey. Any person or entity engaged in an activity within the scope of the VAT law must notify the local tax office where its place of business is located. If there is more than 1 place of business, VAT registration is made at the same tax office at which registration occurred for income / corporation tax purposes.

Different Valuation Types: The Best Valuation Report for Negotiating Property Purchase Price ?

Different Valuation Types: The Best Valuation Report for Citizenship Investment Applications ?

Different Valuation Types: The Best Valuation Report for Setting the Sales Offering Price ?

How to Prevent Inflationary Paper Money Purchasing Power Debasement ?

Money Rebasing Services - Complimentary Strategy Session

Buy the Safe Way & Find Bargains

Sell the Fast Way at the Highest Price

Contact Us...

Learn more by sending a email to info@mytapu.com and include your Telegram or WhatsApp telephone number to receive a free complimentary call back.

Legal Checks on a Property, Ownership, Permits, etc: Due Diligence

Legal Issues for Property Purchases & Sales: Transaction Management

Completion for a Property Purchase or Sale: Conveyancing

Privacy Security - The Right to Privacy is a Fundamental Human Right as stated in Article 12 of the Universal Declaration of Human Rights proclaimed by the United Nations in 1948, with obligations which States are bound to respect. At MyTapu Associates we respect all parties right to privacy, and do not share any information concerning persons nor activities. In addition, all parties interacting with MyTapu are advised to utilise additional protections to ensure their privacy and those they interact with. Simple security protections for privacy enhancing solutions include but are not limited to the following, and the service providers mentioned are tried and trusted: Internet connections by Virtual Private Network (VPN), Nord; Encrypted Email services, Protonmail; Encrypted Voice and Video Call services, Telegram Messenger; Troubleshooting for Privacy Cyber Security, Wilders. Please Note: MyTapu associates may have affiliate marketing engagements with the service providers mentioned.

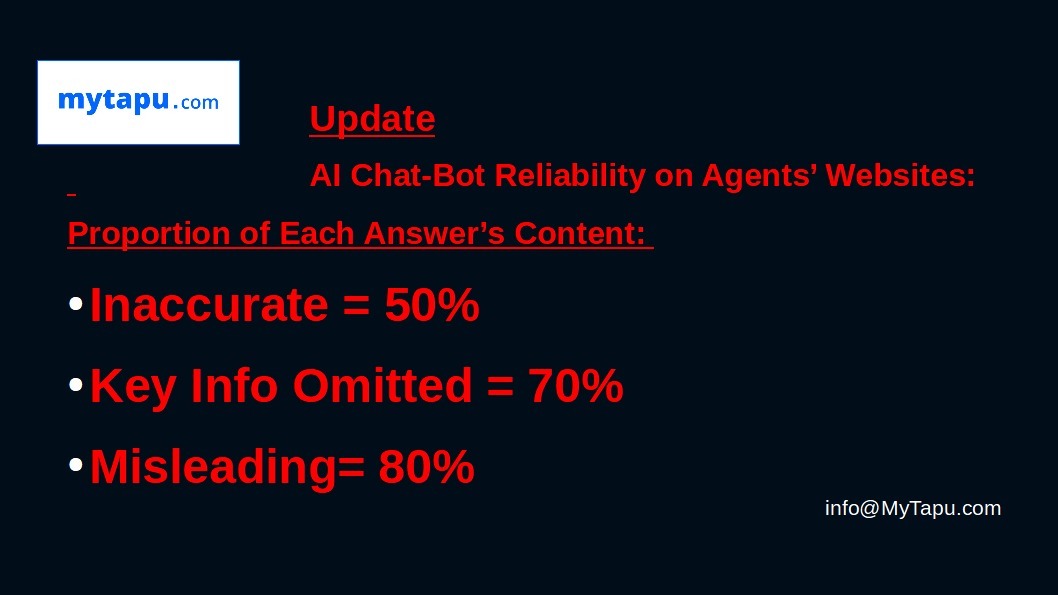

Internet searches are no longer a trusted research source, but instead often result in misinformation and dis-information, and not accurate and reliable information, and should be verified by independent professional advisors that are experts in their specialism., for reasons explained here. Alternative browsers and search engines include, Vivaldi. Tusk, and Yandex.

The Key to Successful Investment in Turkiye....

Share New Insights with Friends !

What MyTapu Clients & Investors say about MyTapu: Customer Reviews.....